The first days at a new job are pretty exciting...until HR hands you the giant book of company benefits to review. Suddenly, you’ve gone from enthusiastic new hire to having to wade through dozens of pages of fine print to understand the benefits that will ultimately affect your paycheck, your financial future, and your wellness.

Intimidated? Don’t be.

As you head into new employee territory, this benefits briefer can help take away the fear factor. Here’s what you need to know:

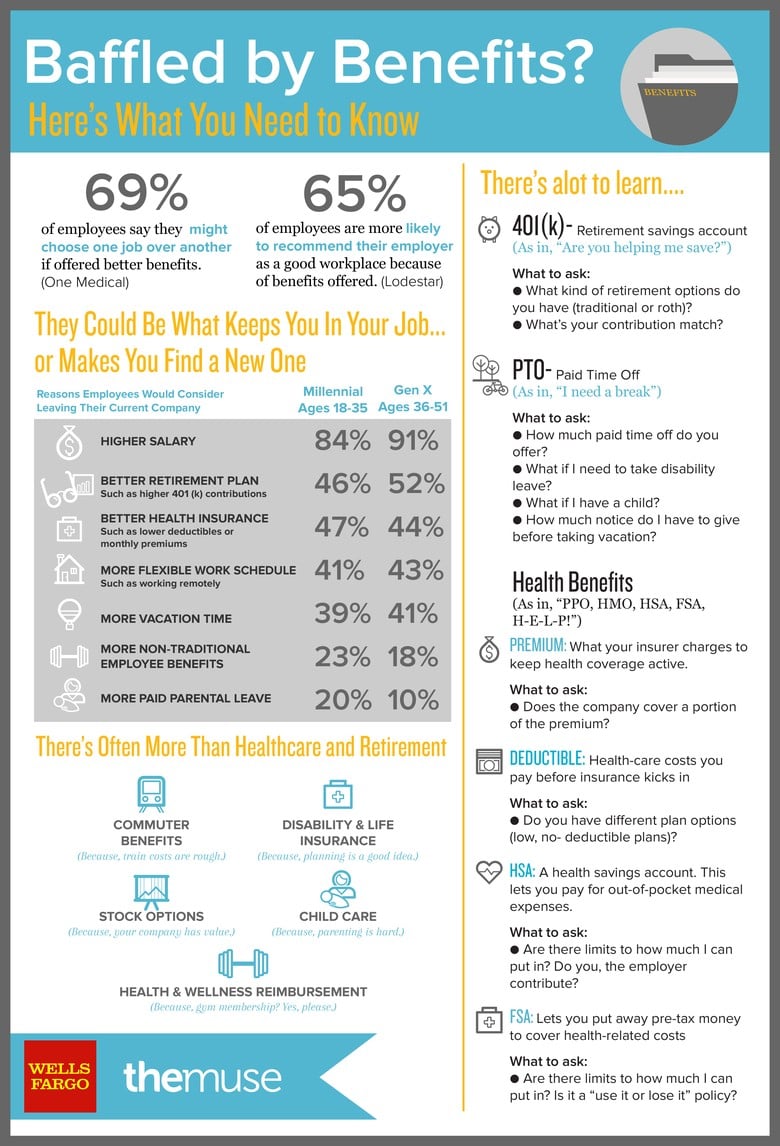

How to Decipher Health-Care Options

The days of simple employee health-care selections are over. Your instinct might be to go with the least expensive tier of coverage, but take some time to examine the following:

Premiums: The amount you pay toward your insurance that will come directly out of your paycheck.

Deductible amounts: How much you’ll have to pay out of pocket before the full coverage kicks in.

Co-pays: A set amount you pay for doctor visits, specialists, hospital visits, and prescriptions. Note that if you choose to use a doctor that is not in your network, you will likely pay more.

What’s covered: Some plans are more generous than others, but most at least allow for a free yearly physical and other preventative care.

If you’re someone with a chronic condition, for instance, it may pay for you to choose a plan with a higher premium but lower co-pays, since you’ll likely save in the long run.

Also, get insight as to how much it will cost to add others if you need to add a spouse or children to your plan.

And don’t gloss over your other insurance options. From dental and vision to short- and long-term disability to life insurance, you may be able to purchase extra protections through your job. Read up on your options to help you decide which are worth going for.

Also your company may have a wellness program that provides discounts for healthy activities (like getting a flu shot or attending a gym) and flexible spending accounts (FSAs), which allow you to contribute tax-free money into an account that can be used toward medical and health related expenses. Just be careful with your FSA—if you don’t use your contributions in a calendar year, they do not roll over. FYI: FSAs are different than HSAs (health savings accounts), which can only be used if you are in a qualified HDHP (high deductible health plan). But, this money doesn't have a deadline and is yours to use for medical and other related expenses.

Read More

How to Fund Your Cushy Retirement

It sounds crazy to think about old age when you’re a young professional, but compound interest and time are a future retiree’s best friends. First and foremost, find out whether your employer does 401K matching contributions. If so, take advantage by contributing at least that percentage from every paycheck; you’re allowed to go up to $18,000 for tax year 2017. (You’ll thank us when you turn 65!)

As far as how to invest in your 401K, you usually are given some preselected choices based on target retirement age, or the amount of risk you wish to take. Although every person’s finances vary, usually, the younger you are, the more aggressive you can be.

Read More

When You Can Actually Use Your Time Off

There’s more to the story than just how many vacation and personal days you get. Is there a waiting period before you can take off? Does time carry over from year to year? Is the company closed on major and not-so-major holidays? Is there bereavement leave? Parental leave? Dig into that section of the benefits handbook, and get answers.

Read More

Other Perks People Don’t Know About

Once the big benefit items are out of the way, you should review other employee freebies and discounts. These may include tax-free public transit and parking allowances, a discounted gym membership, an expense policy for reimbursement on certain items; discounts with certain retailers or vendors through an employee perks program; and tuition reimbursement.

Facing down the benefits book might seem daunting at first, but it’s worth digging into. And if you’re still a little lost, talk to your HR contact or a trusted co-worker (someone who’s been through it before) for help in navigating what’s available to you. After all, you work hard for not only your salary, but your benefits as well.